Subscribe

SubscribeLocalities expecting more tax dollars due to the elimination of the controversial order acceptance test may be sorely disappointed. Application of the final sales tax sourcing regulations, effective as of June 25, 2014 (see 38 Ill. Reg. 14292), may actually increase the number of sales that are sourced outside of the state, such that more sales are subject to the 6.25 percent Use Tax rate instead of the higher Retailers’ Occupation Tax rates that include additional local rates.

Background: Moving from a Test Favoring In-State Sourcing to a Neutral Approach

In previous posts we provided the background on the litigation and policy factors driving this new regulation. See Illinois Department of Revenue Intends to Extend Its Multifactor Post-Hartney Sourcing Regulations to Interstate Transactions; Illinois Regional Transportation Authority Suffers A Setback In Its Sales Tax Sourcing Litigation. Suffice it to say that Illinois sales tax sourcing has been a contentious issue. But Illinois local government units may now find that the revenue impact of these new regulations is worse that the sourcing issues that they attempt to cure: Where the previous regime had tended to source sales to Illinois if part of the retailing activity occurred in the state, the new regulations treat in-state and out-of-state locations equally and attempt to source sales to the location with the best claim on the retailing activity.

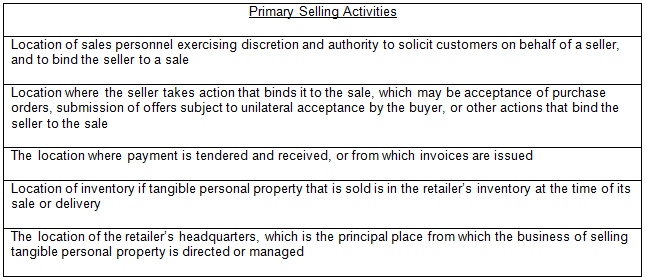

Step One: Can a Location Claim at Least Three of Five Primary Selling Activities?

The first part of the test looks to five primary selling activities. If at least three of the primary selling activities occur in one business location, then the sales are sourced to that location. See 86 Ill. Admin. Code 220.115(c)(1), (2). (Note: These sourcing regulations are codified in parallel under several chapters of the Illinois Administrative Code. See 86 Ill. Admin. Code 220.115, 270.115, 320.115, 370.115, 395,115, 630.120, 670.115, 690.115, 693.115, 695.115. For convenience we will cite to 86 Ill. Admin. Code 220.115, but parallel provisions exist in the other regulations.) The primary activity factors are as follows:

Broadly speaking, the primary selling activities would likely result in headquarters-based sourcing as long as the business has a centralized headquarters with personnel that have the authority to bind the seller and personnel issuing invoices and processing payments. Additionally, there appears to be an overlap between the first two activities: If salespersons have authority to bind the retailer to a sale, then it would seem that the second factor, where the binding action takes place, would also be implicated.

Step Two: If No Location Has a Majority of Primary Selling Activities, then the Headquarters and Inventory Locations Compete for Sourcing Based on Primary and Secondary Factors

Assuming that no single location can claim three primary selling activities, the test then turns to the second step, in which both primary and secondary selling activities are considered in determining whether the sales should be sourced to the headquarters location or the inventory [...]

Continue Reading

read more

")

")