While the state treatment of global intangible low-taxed income (GILTI) was on the mind of many taxpayers, most state legislatures that enacted legislation in 2018 focused on the state treatment of foreign earnings deemed repatriated under IRC § 965, leaving the state treatment of GILTI unclear in many states. That said, of the states that enacted legislation addressing GILTI, very few have decided to tax a material portion of GILTI.

In states that did not address global intangible low-taxed income through legislation, a lack of clarity in the state laws created an opportunity for the STAR Partnership to seek favorable administrative guidance on the treatment of GILTI. The STAR Partnership pursued that opportunity in a number of states, as discussed in more detail below.

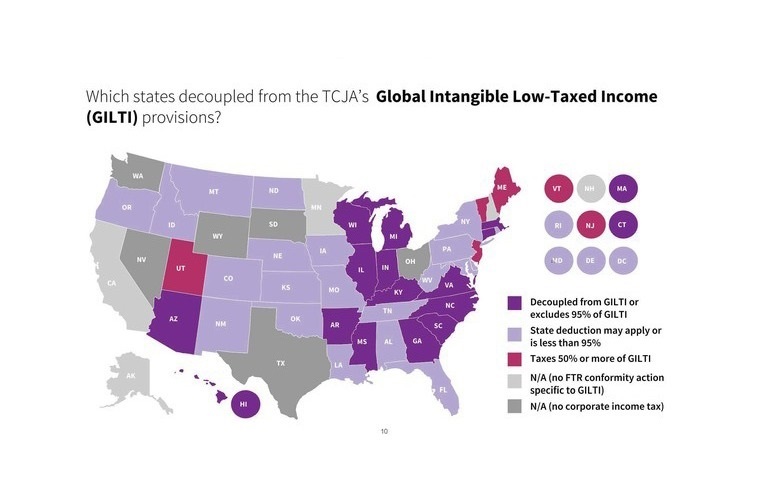

Set forth below is a map illustrating the states’ 2018 legislative responses to GILTI.

The STAR Partnership expects GILTI to be a very important issue in the 2019 legislative cycles, and plans to continue to advocate for the exclusion of GILTI from the state tax bases either through legislation or administrative guidance.

2018 STAR Partnership Success Stories Related to GILTI

Connecticut: Connecticut provides a dividends-received deduction for deemed dividends that, based on guidance from the Connecticut Department of Revenue Services, applies to GILTI. A bill proposed by the Connecticut legislature would have deemed 10 percent of the dividend income to be a non-deductible expense attributable to such income. The STAR Partnership prepared policy and technical talking points and worked with local advocates to support the legislation that was ultimately adopted and contained an expense attribution percentage of only 5 percent.

Hawaii: The STAR Partnership prepared policy and technical talking points and worked with local advocates to support Hawaii’s decoupling from the GILTI provisions in IRC § 951A. When legislation was passed, Hawaii did decouple from IRC § 951A.

Indiana: The STAR Partnership prepared policy and technical talking points and worked with local advocates to support Indiana’s exclusion of GILTI from the tax base. Indiana did enact legislation providing a 100 percent deduction for GILTI, provided the taxpayer owns at least 80 percent of the foreign subsidiary.

Kentucky: The Kentucky legislature passed legislation in response to federal tax reform under which it was unclear whether the state’s dividends-received deduction applied to GILTI. The STAR Partnership requested a Technical Advice Memorandum from the Kentucky Department of Revenue providing that GILTI would be treated as dividend income and eligible for Kentucky’s dividends-received deduction. The Department agreed with the STAR Partnership’s arguments that GILTI should be treated as a dividend and issued the guidance requested by the STAR Partnership in August 2018.

Massachusetts: The STAR Partnership advocated for decoupling from the GILTI provisions in IRC § 951A or providing a deduction for GILTI. The Massachusetts legislature did enact legislation providing a 95 percent deduction for GILTI.

North Carolina: The STAR Partnership prepared policy and technical talking points and worked with local advocates to support North Carolina’s decoupling from the GILTI provisions in IRC § 951A. The North Carolina legislature did enact legislation providing a 100 percent deduction for GILTI.

Oklahoma: Due in part to the advocacy efforts of the STAR Partnership, the Oklahoma Tax Commission stated it will issue regulations that would provide that GILTI is treated as dividend income and allocated to the taxpayer’s state of commercial domicile.

South Carolina: The STAR Partnership prepared policy and technical talking points and worked with local advocates to support South Carolina’s decoupling from the GILTI provisions in IRC § 951A. The legislature did pass a statute decoupling from IRC § 951A.

")

")